By Illustrator T. Allom, Engraver J. Tingle - History of the cotton manufacture in Great Britain by Sir Edward Baines,, Public Domain, https://commons.wikimedia.org/w/index.php?curid=9430141

The future is already here — it’s just not very evenly distributed. – William Gibson

Nota bene: Readers familiar with Machina Cogitans will find that this essay takes a different approach; rather than philosophical inquiry into the nature of AI and its relationship to humans and society, the focus here is on the economic and market structure implications of technological revolutions generally and AI specifically, and on their application in an institutional investing environment.

Abstract

Conceptual paradigms do not progress in a linear and orderly fashion. Scientific paradigm shifts occur with punctuated regularity, as do the techno-economic paradigm changes brought about by technological revolutions. Carlota Perez provides a framework that describes how technological revolutions diffuse through the economic, institutional, and technological spheres of the incumbent techno-economic paradigm. Financial capital acts as the driver of rapid diffusion during the installation period; the subsequent turning point marks the institutional and societal recomposition that precedes the deployment period, where production capital takes over. While most investors myopically focus on the risks associated with bubble dynamics, they misprice the opportunities arising from the structural reorganization of the economy itself: markets perceive the new topology too slowly, and it is within this gap that mispricing persists. This mispricing we call innovation premia. Innovation premia distinguishes itself from the purely speculative premia associated with financial capital during the installation period; it seeks to anticipate, and participate in, the new topology within which production capital will be deployed. Harvesting innovation premia can take many forms and appears in market, organizational, and behavioural dimensions.

In his highly influential book, The Structure of Scientific Revolutions (Kuhn 1970), Thomas Kuhn characterized the progress of scientific thought as being punctuated by epochal paradigm shifts in understanding; shifts he termed scientific revolutions. During the transition period from one paradigm to another, both paradigms co-exist, albeit incommensurately. That is, the new paradigm is not simply an advancement or extension of the existing framework, but is fundamentally novel in that different standards of explanation, language, and evidence arise. As such, discourse between the two paradigms is itself fraught with misinterpretations and, at times, rancour, as proponents of each paradigm, old and new, seek either to maintain the status quo or replace it, each of whom arguing and defending analysis from within their own paradigm, when it is the paradigm itself that is up for debate. Evidence, often assumed to be a neutral arbiter within science, can no longer remain neutral, as evidence itself becomes interpreted differently between the two paradigms. It was only ever a neutral entity within its own paradigm. Indeed, even the avenues of legitimate scientific inquiry are bound to each paradigm: which questions can be asked, funding for instruments, and what qualifies as an acceptable explanation. This period can sometimes be characterized by an increase in radically differing interpretations of the exact same evidence.

For the new paradigm, it must overcome an entrenched structure of academic and institutional inertia that has developed around the old paradigm, and which is unable to adapt or recognize the new. Yet, as anomalies and discrepancies accrue, a crisis develops.1 This crisis becomes both pall-bearer for the old and midwife to the new paradigm; it highlights the limits of the old paradigm while simultaneously illuminating the new paradigm’s frontiers. Researchers, increasingly frustrated with the failings or limits of the old paradigm, seek new solutions.

As the new paradigm increasingly demonstrates its superiority over the old paradigm, and the leaders from the old paradigm eventually retire,2 the old paradigm withers away and is replaced by the new. Textbooks are rewritten, a new generation of students and professors is trained in the new approach, and most of science concerns itself with systematically applying the new paradigm throughout its discipline. In other words, once the new phase begins to take hold, the dominant work of science is not innovation, but the application of the new paradigm and its implications. Indeed, scientists must become wholly committed to the new concepts so as to apply them as broadly as possible. To be clear, this is not a bug, but a feature of the scientific system.

Nonetheless, such focus comes at a cost.

Those steeped in the language and concepts of the current paradigm can fall subject to very real institutional inertia, as both institutional structures and personal incentives can be slow to adapt, or even resistant or blinded to it. Such forces can range from something as simple as the education available, to current funding bodies’ mandates, or to basic professional incentives. Yet, as history and Kuhn show us, these entrenched pathways of thought are replaced by the next scientific revolution. One of the core insights from Kuhn is that it is not only younger scientists, but also those simply less invested in the current paradigm who bring about scientific revolutions. Whether it be due to increasing frustration at the accumulation of anomalies in their own research, or to researchers from other disciplines, at some point a critical mass of evidence and adherents to a new paradigm will arise.

Structural Origins of Innovation Premia

With artificial intelligence, a new paradigm shift is upon us. This paradigm shift will profoundly impact core centres of economic production and is already causing, or is about to cause, significant disruption to wide swaths of the economy and society. With Waymo, self-driving cars will taxi you, call centres no longer require armies of employees, programming is being automated, and so on. In institutional settings, teachers now have to deal with students cheating via AI,3with downstream effects on the capacity for independent thought amongst the next generation of the labour force. Similar to the shift we saw with the rise of the internet, this technological revolution is expected to have wide economic reach and impact, and likely more so. As AI diffuses into more of the economy, the economy will begin to rewire itself, unravelling the old connections and creating new ones.

As society structurally reorganizes to accommodate this new technology, dislocations between the old and new paradigms will proceed at differing paces across different facets of the economy and society as the new technology diffuses through the system. In much the same way that Kuhn describes academic inertia as resistant to change due to long-term investment in large-scale experiments, sunk costs in intellectual capital, funding mandates, etc., similar sectors of the economy and society will be slow to adapt and change. To be clear, this is not an indictment of those institutions, but rather a statement of fact about them: they were explicitly set up to promote stability for the long term following the last revolution. As these two paradigms co-exist, dislocations will continue to propagate throughout the system as adoption of the new paradigm becomes more rapid. Nonetheless, the replacement of technology alone is not sufficient for a techno-economic revolution. What is required is the accompanying structural change in society and the economy to maintain the new paradigm, whatever that may be. As such, there is a period of both confusion and radically differing interpretations of the same data by investors and regulators alike.

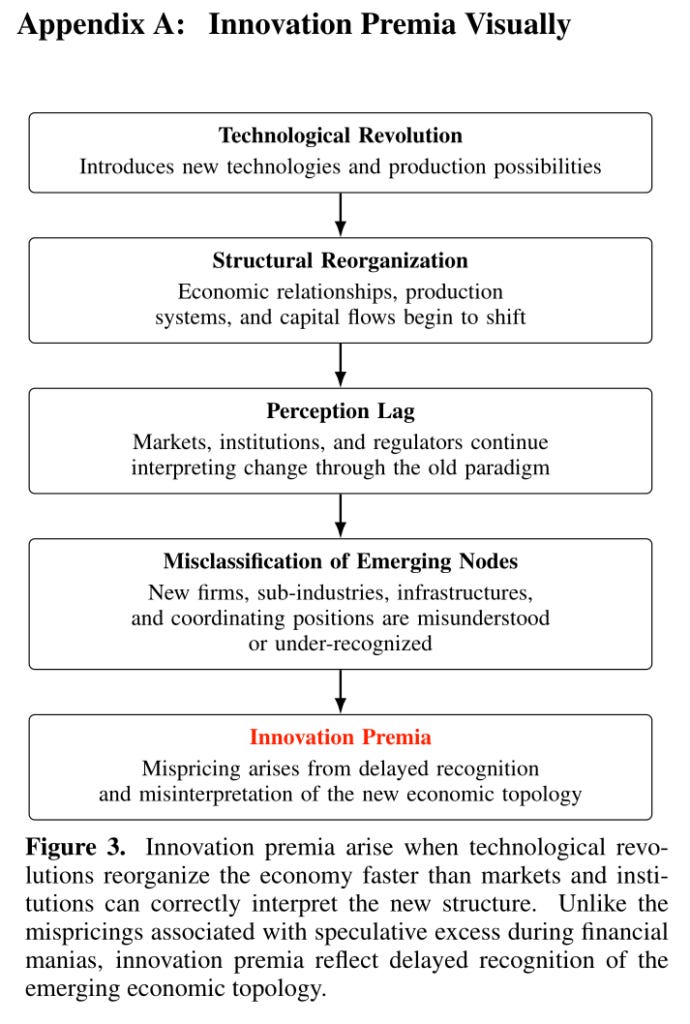

Misinterpretation of the technological revolution widens as financial capital moves speculatively and unevenly, often before the production system stabilizes, while institutions and regulators are still trying to interpret the changes within their current framework. Out of this, a profound dislocation between the actual economy and the markets’ perception of it grows. Within this space arises what we call innovation premia: the mispricing that emerges when markets misinterpret the structural reorganization of the economy during technological revolutions. The critical point is that markets are not merely mispricing a new technology per se, but rather that they are mispricing the new economic topology itself and, with it, where value will ultimately reside within the emerging production system’s new hierarchy.

While Kuhn focused on scientific revolutions specifically, the structural framework for paradigm shifts can be applied more generally. A natural extension is that scientific revolutions can also precipitate technological revolutions, and vice versa.4 Perez (2002) explores this application of a Kuhnian-style framing of revolutions to the economy and society, which she terms techno-economic paradigms, in her book Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. More specifically, she explores the intersection at which clusters of technological innovations, institutional change, and financial capital emerge and, importantly, the role financial capital plays in accelerating technological revolutions while also contributing to the wild mispricings characteristic of boom bust dynamics through speculative excess.5 Leveraging Perez’s framework to define the mechanisms of techno-economic revolutions, we can then interpret these shifts as changes in the topology of economic networks from which innovation premia arise.

Techno-Economic Reorganization

Carlota Perez provides us with a comprehensive review of the characteristic phases associated with technological revolutions and the role financial capital plays within them (Perez 2002). Moreover, she articulates the concept of a techno-economic paradigm.6 Such paradigms establish the societal norms of best practices with existing technology, standard cost structures, accepted benchmarks of comparative advantage, production organization and labour structures, the institutional and regulatory frameworks under which companies operate, and so on. We see within Perez’s techno-economic paradigm a similar normative latticework of institutional and private modes of operating that define legitimate inquiry, valid investment, and economic interpretation Kuhn characterizes for scientific revolutions. Techno-economic paradigms are not simply the introduction of a new technology, but rather the organization of an economy around a foundational technology or mode of production that has diffused throughout society, establishing financing, labour, and educational norms. As such, a techno-economic paradigm is the network of interlocking spheres of society and the economy that provide coherence and stability; a technological revolution is the process that rewires the current paradigm into a new one.

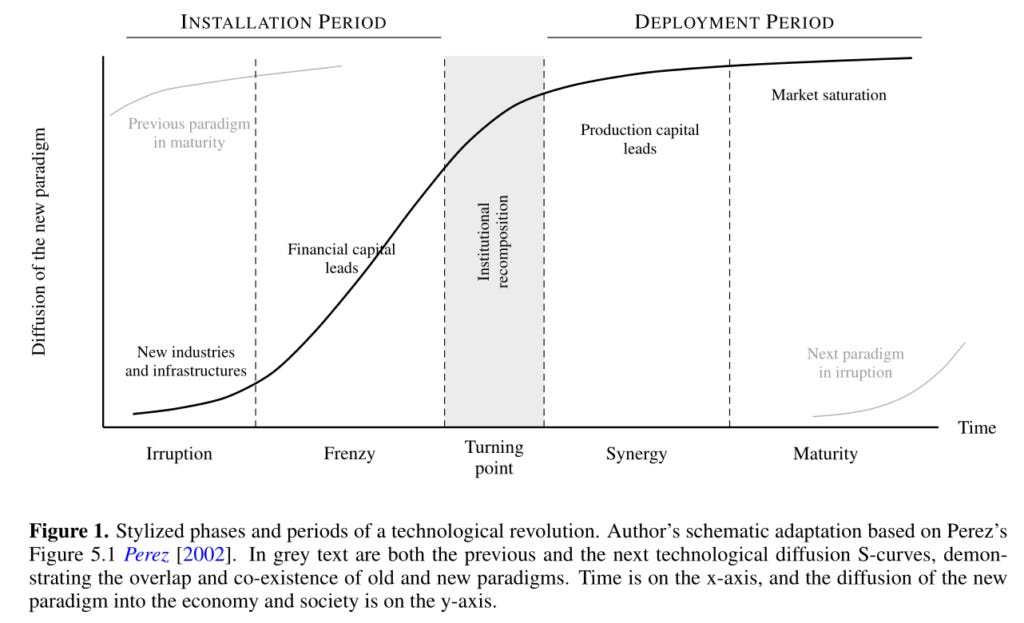

By analyzing the dynamics of the economy and capital over historical technological revolutions, Perez was able to identify and interpret characteristic epochs commonly associated with each revolution. An understanding of this framework and the mechanisms at play in technological revolutions, in both the economy and broader society, will provide the necessary scaffolding upon which innovation premia stands.7 When viewed as a full cycle, technological revolutions exhibit similar epochs of financial, institutional, and economic reorganization. While not all historical revolutions follow the exact same timeline, they do adhere to a regular cadence of activity. In her framing, there are two distinct capital dominant periods, Installation (financial capital dominant) and Deployment (production capital dominant), separated by a shorter, less readily delineated Turning Point, during which the lagging institutional and societal reorganization occurs. See Figure 1 for a stylized representation of a technological revolution cycle.

Installation

As the name suggests, the installation period sees a new technology diffuse into the economy. What differentiates the new technology from simple improvement over existing technology is the potential for it to change the techno-economic landscape. Going from Lotus 1-2-3 to Excel is not the herald of a technological revolution; switching from steam to electricity is. Often such new technology is not fully understood in its early development, even by its inventors themselves. Edison, for example, thought the phonograph was going to be used primarily to record wills, not to change the nature of the music industry. As such, the new technology is developed at the fringes of the current financial ecosystem in an exploratory fashion.

Financial capital that has been building up in the current techno-economic paradigm, still in its maturity phase, seeks out new avenues of risk into which it can be deployed as returns begin to plateau. The emergence of a new technology provides the opportunity; however, this same novelty limits the sources of capital willing to take on higher risk. Naturally, venture capital and entrepreneurs tend to be first movers in deploying financial capital to help develop the new technology through experimentation and speculation. In this period, financial capital, which tends to be short-term, liquid financing, is necessary to provide the momentum required to accelerate the new technology’s adoption over the current paradigm. The influx of this capital starts slowly and then becomes a flood, threatening stability in the irruption and frenzy phases of the installation period. Stability, in the context of a technological revolution, refers to the degree of disruption to the current techno-economic paradigm, as well as to the speculative intensity of financial capital within the system.

In this model, the installation period has two phases, both of which are dominated by the influence of financial capital. The first phase is the irruption of the new technology, where once-sidelined financial capital begins to see the possibility of the new technology. Here, new entrants begin to invest in the space, and what was once a trickle of financial capital begins to flow more readily. While uncertainty remains around the final form of the new technology, investors are generally optimistic about the potential the new technology holds. As the optimism around the new technology grows, early-stage infrastructure begins to form around the new technology to facilitate its further experimentation and its potential to scale into the wider economy. Nonetheless, there remains ambiguity on what the new techno-economic structure will eventually coalesce into. As such, while capital flows continue to increase, they do so at a stable rate. Capital commitment has now begun in earnest.

The shift to the frenzy stage is marked by financial capital flooding into the system. Here we begin to see a change in investor behaviour where conviction in the new technology outpaces understanding of it. As capital pours in, multiples expand rapidly and detach from fundamentals. Infrastructure to facilitate the long-term investment in the new technology begins to scale out with a blinding urgency. Competition between firms developing the new technology becomes more intense. Speculation dominates capital flows. And yet, it is not completely irrational either: a major paradigm shift is underway. Here investors have correctly identified that a new technological paradigm is emerging, but do not yet understand how the resulting techno-economic structure will be organized. Late movers, seeking to participate in the new technology, look for ways to participate in the technological revolution. As the fundamentals of companies driving the technological revolution become unpalatable for many investors, new speculative instruments arise to facilitate exposure: the new technology inspires innovation in the financing space as well. Innovation breeds innovation. The winds have changed, but onto which shores will we arrive?

Turning Point

Crash.

As the forces associated with the frenzy of the installation period culminate in an economic correction, the release of tension accrued in the system from the flood of financial capital becomes inevitable. The boom-bust dynamics that signal the end of the frenzy are necessary for technological revolutions and indicate we have arrived at the turning point. But to simply call it a bubble misses the point of what distinguishes technological revolutions altogether: the entire techno-economic paradigm is in the midst of restructuring itself into a new form. A market crash is only one part of that change. To see the full picture, we need to cast our gaze more widely to appreciate the scope of transformation taking place.

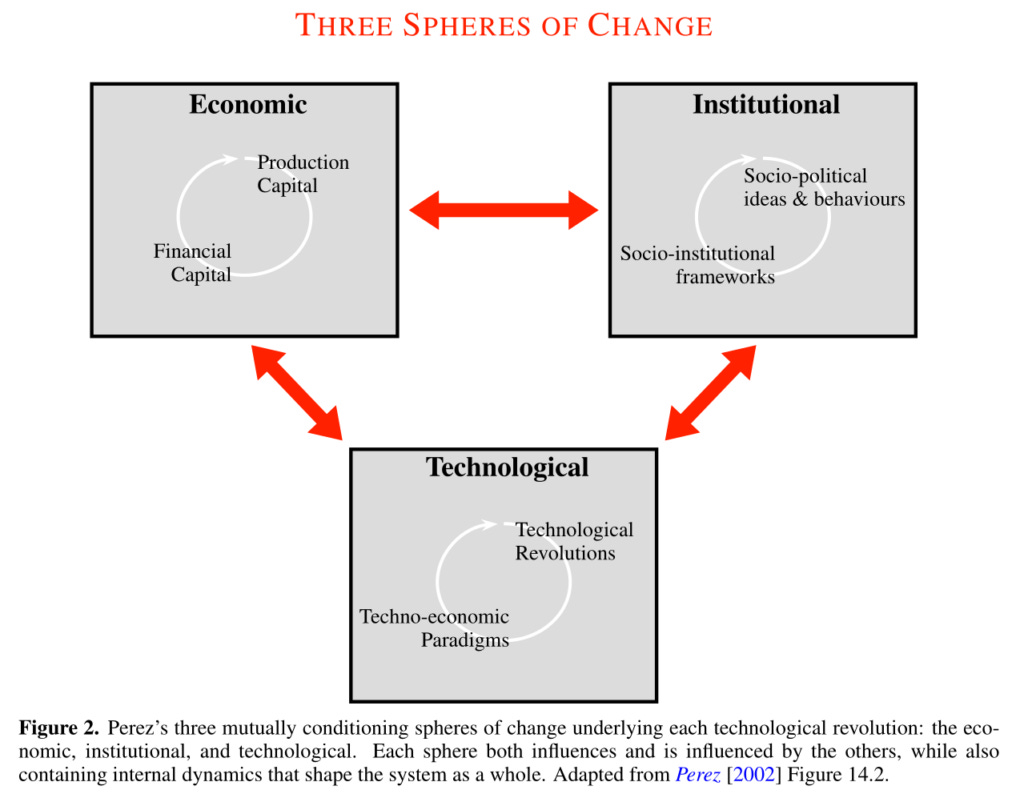

There are three dominant spheres where transformation manifests during technological revolutions: the Economic, Technological, and Institutional (Figure 2). As the new technology propagates through each of these domains, its diffusion is limited to the pace at which each domain can accommodate the changes. Until now, the economic domain has been swiftly deploying capital as the technological domain continues its rapid pace of innovation. All the while, the institutional domain is still in the process of trying to understand the changes to the emerging techno-economic structure before it can properly respond.

Financial capital, having provided the necessary funding to develop the technology and help invest in its new infrastructure, collapses under its own weight. This, of course, is unsurprising, as it is the innate liquidity of financial capital that allows it to move to support the new technology, which also allows it to be withdrawn just as quickly. Here, the new speculative financial instruments, often poorly understood, implode most dramatically during the turning point. Nonetheless, we need to recognize the fact that the new technology is genuinely establishing a new techno-economic paradigm. It’s not tulips.8

Along with compressing equity multiples, economists begin to recognize that a powerful reshaping of the labour force is necessary to accommodate the new techno-economic paradigm; evidence that the labour force is beginning its metamorphosis becomes hard to ignore. In addition to the changing shape and skills required of the labour force, new geographical centres of production form: labour is not only re-skilling, but also potentially migrating. Networks of labour are reorganizing around the new technology while the existing structures begin to disintegrate. Consider the changes brought about by the industrial revolution in how labour was structured, mobilized, situated, and, ultimately, employed. The disruption in this arena leads to political and societal unrest, further compounding the uncertainty brought on by the wealth destruction as the markets crash. As frustration mounts, investors and society alike clamour for institutions to rein in the excesses that caused the crash. Paradoxically, institutional intervention prior to this is almost guaranteed to be ineffective, as there will be no evidence of how the new technology would be used, or which structures will emerge in the new techno-economic landscape. Now, however, the strain in the system has reached levels high enough to overcome the inertia necessary to move institutions into action.

During the turning point, a culling of companies with unsuccessful business models occurs. Whether through their inability to adapt or to predict the direction of the new technology, it amounts to the same thing. Those with sound business models, and who are able to perceive the new paradigm, establish the dominant design of production within the emerging techno-economic paradigm. With this clarity, institutions are able to mediate the reintegration of the other spheres and facilitate the orderly transition to production capital coming to the fore to build out the infrastructure for the new techno-economic order.

Deployment

Having come through the turning point, we now enter the deployment period of the technological revolution. Similar to the installation period, the deployment period is divided into two phases: synergy and maturity. With the crash and uncertainty of the turning point behind us, the process of recoupling and coordinating the economic, technological, and institutional spheres into the new techno-economic paradigm can begin in earnest.

With increasing regulatory certainty and the structure of the new paradigm now coming into focus, production capital mobilizes to build out the new infrastructure required during the synergy phase. In this phase of build-out, the foundational infrastructure, regulations, and capital-raising facilities are rapidly developed to meet the current and future demands of the new techno-economic paradigm taking hold. Diffusion of this process, however, varies across industries and regions; those with direct exposure are prioritized before supporting and ancillary businesses. Indeed, many industries will need to be reorganized and classified as the new technology transforms the sector. For example, consider how the media landscape evolved during the introduction of the internet. While this process unfolds, improvements and production efficiencies also come into peripheral view: the whole system becomes more coordinated and productive as each new component recouples into the new paradigm.

This is not to suggest that the techno-economic reorganization is without its challenges. With the new paradigm taking shape, cleavage points separating the old from the new arise. We see new leadership take hold as firms modernize at different paces and with differing success; regional divergence manifests as new centres of production come online; and the labour force is split as technical fluency with the new technology reveals fault lines separating those who have acquired the new skills from those who have not. Those actors who are able to understand the new paradigm’s potential itself are further distinguished. Nonetheless, as familiarity with the new paradigm diffuses into more arenas of the economy and society, we approach the final phase of technological revolutions: the maturity phase.

The wave of innovation brought on by the new technology has finally reached all shores: the new technology becomes the dominant paradigm. All sectors and aspects of the economy and society have adapted to the new technology, and the adoption of best practices is integrated throughout the system. As the novelty of the new technology recedes, so too do the opportunities to innovate. In a similar fashion to the scientific revolutions of Kuhn, the new technology has been applied throughout society, but the applications for it become ever more scarce as time goes by.

Production gains, previously significant during the synergy phase, now become modest. So too do the returns. Here we find ourselves entering a slow process of ossification as efficiencies from the new paradigm exhaust themselves. Capital becomes less productive in the now dominant paradigm, and a new technological revolution is required. Throughout this period, dominated by production capital, financial capital has been accruing. The frustration of scientists with the limits of the new scientific revolution applies to investors as well: frustration with lack of returns sees financial capital begin to mobilize and seek out new avenues to explore for investment. The next technological revolution is on the horizon.

While I have attempted to cover the core ideas of Perez in the above sections, they are heavily abridged and paraphrased. Nonetheless, it was necessary to review her ideas relating to the dynamics and the role of capital in technological revolutions, as well as the scope of techno-economic reorganization, in order to lay down the necessary foundation for an understanding of innovation premia.

Rewiring the Machine

Now armed with a broad overview of how the structure of technological revolutions unfolds, we can now move on to a more interpretative frame. An obvious framework to apply is that of network theory, which provides both the language and quantitative tools that can be brought to bear to further interpret the mechanisms described by Perez.

It is natural to describe a techno-economic paradigm as being the topology circumscribed by an interconnected network of networks. At one level, we could consider the reciprocal relationships of the Economic, Technological, and Institutional spheres as described in ; and at another, we could focus on the intra-network relationships within a single sphere, such as the economic. However, for our purposes, which are expositional, we will adopt a simplified approach and leave it to the reader to determine the intricacies of a more formal implementation, should they so desire.9

Nodes, Edges, and Structure

To make matters more concrete, we briefly introduce some basic language from network theory. In general, networks consist of nodes and edges, where nodes represent the entities of interest and edges define the relationships amongst them. Nodes, in our context, can be firms, infrastructure, and other economic agents; edges are the channels through which information, capital, and production are coordinated. These relationships may be symmetric, for example, a path between two cities, but need not be. Non-symmetric relationships can arise, such as differences in upload and download speeds.

Relationships may also vary in depth, corresponding to paths of differing length through the network. For example, a firm may be directly connected to its suppliers, but also indirectly connected to its suppliers’ suppliers, and so on. It is often through these longer paths that the true structure and influence of the network reveal themselves. Similar to mental models of second- and third-order thinking, multi-depth networks allow one to invert the relationship such that, instead of the node of interest (focal node) projecting the consequences of its actions outward, it acquires and consolidates information and changes arising at the outer reaches of the network to itself.

A special class of networks, often referred to as semantic networks or knowledge graphs, provides a representation of heterogeneous relationships and offers one avenue through which investors may examine the structure of such systems. Moreover, they allow disruptions at the network’s less-integrated periphery to be incorporated more readily, reducing the lag inherent in conventional channels through which this information would otherwise reach the focal node. Within such networks, the relationships become as important as the underlying nodes, potentially more so. Semantic networks allow for new topologies to be explored in a dynamic way, particularly where relationships are less well integrated, lending themselves to the interpretation of the ontological properties of the system; the topology itself becomes a new source of insight and interpretation.

Economic Mapping

Before we can move on to discussing changes to the topology of the techno-economic paradigm, we first map economic entities onto the nodes and edges we have just described to help anchor the wider discussion within a familiar landscape.

The most tangible example is infrastructure, where ports, distribution centres, and energy infrastructure are nodes. Their intersecting network of shipping routes, railways, energy lines, and highways constitutes the physical edges in this system. We can characterize any such entity by examining various measures of node centrality. Consider a port: it may exhibit high betweenness centrality, as it connects many origin and destination points for goods. It can also have high degree centrality based on the number of routes (edges) connected to it. If it is well positioned, it may also have high closeness centrality, as measured by the length of the routes connected to it. Moreover, it may exhibit prestige centrality based on the status of its neighbouring nodes. In this sense, centrality describes the importance of a node within the network; removing a highly central node reduces the efficiency of the network overall. It is not simply the number of connections that matters, but how indispensable that node is to the network. One can carry out the same exercise for energy infrastructure if one so wishes. The main point is that interpreting the port system using network theory provides a language to describe meta-properties of the network that are themselves of economic importance.

While infrastructure provides a tangible example of network topology, we can extend the same analytical framework to firms. In this case, the network complexity increases as a firm is embedded as a node within supply chains, capital networks, and information flows more broadly. For firms, public or private, where such data are available, relationships associated with financing, such as venture capital deployment, can be examined. Partnerships, suppliers, customers, regional, industry, or purely statistical relationships can likewise be mapped. Within these networks, we can carry out analyses related to the robustness of their supply chains and their relative importance and, in some instances, estimate their negotiating power based on their centrality. In Japan, for example, the Toyo Keizai Shareholder Data provides detailed information of the cross-shareholding relationships, ostensibly employed by firms in Japan to solidify long-term relationships, deter hostile takeovers, and reinforce loyalty amongst members of their respective Keiretsu, a type of business network unique to Japan.10 We could go on.

None of this, of course, is novel territory. Most sophisticated quant shops have already invested in the technology required to construct directed, multi-dimensional, multi-depth networks and knowledge graphs in the pursuit of alpha. A common strategy is to define a network of relationships, such as suppliers, and use this structure to aggregate information for each of its nodes. For example, analyzing how momentum signals from a company’s suppliers propagate to the focal company can provide a measure of its group momentum, which can in turn be predictive of the focal company’s self-momentum. In practice, this type of analysis often stops at the first node out or is applied only to the simplest factors. For the most sophisticated quants, such networks are generated over multiple dimensions (customers, suppliers, partners, among others), with multiple signals (fundamentals, revisions, sentiment, etc.), and at multiple levels of depth. This additional complexity, albeit onerous to build, provides a comparative advantage to those willing to invest in such technology, akin to the early adoption of ticker tape devices: an early warning system for information originating at a distance. Yet the dominant use case remains the aggregation of information for decision making about the focal firm, rather than insight into the structure of the system itself.11

But understanding the nature of the topology itself has economic value, even if only through reframing how one interprets current market dynamics. By way of example, consider the new high-centrality nodes with Microsoft (MSFT) as an emerging central hub. MSFT has multi-billion-dollar equity stakes and significant cloud partnerships with OpenAI and Anthropic. At the same time, hardware providers such as NVIDIA, Broadcom, and Taiwan Semiconductor Manufacturing Company are supplying the chips that power the cloud architecture required by the new technology. Here we see an example of financial capital in the early installation phase funding both technology development (MSFT to the AI providers) and the infrastructure build-out (via hardware providers supporting MSFT). A new dense cluster is forming in which MSFT is effectively acting as a large-scale venture capital node, deploying capital in a manner more characteristic of the installation phase than of mature production capital. In this case, financial capital is rapidly rewiring the software and hardware space. The question for the investor is whether this emerging topology is being priced as deployment-phase infrastructure or as installation-phase capital.

Mapping the Territory

Connecting it back to Perez, we see that a techno-economic paradigm is a topology; a topology of reciprocally acting and interlocking spheres through which capital flows. Technological revolutions, as such, are the processes associated with rewiring that topology. From the models employed by investors to the inertia of institutions resistant to change, lags are introduced into the system that create dislocations between the reality of the emerging new topology and the market’s perception of it: their map is not the territory. Financial capital, in accelerating the rewiring, compounds this gap further still. Within this space resides opportunity.

Mispricing the Revolution

With the quantitative tools provided by network theory, we are now in a position to make the connection to Perez’s technological revolutions more explicit. Characterizing the economy as a multi-dimensional, multi-depth, directed network of relationships is a natural extension to adopt. Expanding to the wider techno-economic paradigm, nodes in the economic network are influenced by the regulatory and institutional milieu in which they reside, and many firms directly participate in the research underpinning the technological revolution. For our purposes, however, we will focus on the economic sphere as our primary vantage point from which to interpret technological revolutions and will highlight where the technological and institutional spheres intersect with it when warranted.

Into the Gap

Investors love stability. When market and geopolitical forces are well behaved, model assumptions can reasonably be treated as stable over the investment horizon and, thus, investors’ expectations about returns. Implicit in this is that the structure of the techno-economic paradigm is also stable, as is characteristic of the Maturity phase. Yet, as Perez shows us, that is only one part of the cycle for technological revolutions; the Installation period and Turning Point are periods of change, specifically of structural reorganization.

Therein lies the rub.

The key tension resides in the disparity between the stability of economic assumptions and the actual pace of change occurring in the real economy during technological revolutions. As the topology changes in response to the new technology diffusing throughout the system, many market models continue to apply an old topology. Moreover, the pace of this changing topology, as Perez’s model shows, accelerates as financial capital acts as a forcing mechanism, driving the system into a new equilibrium. This process sees new nodes emerge, legacy nodes fade, and new edges form; centrality shifts as the new techno-economic paradigm takes hold.

Asynchronous diffusion of the paradigm further complicates navigation of the new topology. New geographical centres arise and prosper, while older regions come under distress as the new technology propagates, taking with it capital that formerly sustained the local economy. Even those adopting the new paradigm do so at differing rates. Adoption of the new techno-economic paradigm does not proceed in a coordinated or sequential fashion, but is instead jagged and haphazard. Within the gaps that arise between the old and the new, innovation premia can be found.

Mechanisms of Mispricing

Some clear mechanisms can be identified that generate mispricing, as well as contribute to its persistence in the market. While not exhaustive, three dominant modes can be readily identified: firms being evaluated through legacy frameworks; emerging importance being under-recognized or slow to be adopted; and the actual topology of the economy changing before classifications, often institutionally defined, do.

An obvious example of where models lag the techno-economic paradigm shift is found in the definition of a factor like Value over the last two decades. Traditional measures focused on tangible assets as being foundational to the inherent value of a company, for example, Book-to-Price measures. However, when social media, streaming, and other tech-related firms emerged, where the number of subscribers mattered more than a physical plant, many investors struggled to coevally capture this fundamental change when valuating such firms. Intangibles became more important in some industries than others. While conceptually the notion of seeking undervalued firms to buy persists, the definition of what Value is was no longer stable.

Recognition of the importance of the new technology also leads to mispricings arising from adoption strategies, or lack thereof. In some instances, a genuine lack of understanding of the new technology and its application can lead to resistance to adoption altogether. For others, adoption may be slow for a variety of reasons, be they regulatory constraints, lack of conviction, or self-serving; it amounts to the same thing: differential adoption of the new technology, both inter- and intra-industry.12

Last, one of the most recognized category errors is related to industry mapping. As a general rule, GICS classifications, defined and approved by committee, are typically the last to know that a company is misclassified. For quants, this can be especially pernicious, as their investment universes often number in the hundreds to thousands. When attempting to neutralize industry or sector effects with misclassified companies, you are comparing apples and oranges, potentially leading to inadvertent tilts in your portfolio. This, however, is widely known, and most risk model providers now offer dynamic industry mapping versions. Indeed, the notion of companies being singly categorized is also now commonly addressed through fractional industry exposures.

Not only do these mechanisms generate mispricings, they sustain them. Models lag in both definition and adoption; even as new models emerge, early movers gain an advantage with frameworks better suited to the new paradigm. Institutional lag, as Perez discusses, is expected, as the wider impacts of the technology are still being understood. This creates the conditions for regulatory arbitrage, where participants effectively bet on regulators adopting policies in their favour. Finally, as production capital is constrained by its less liquid and less risk-seeking nature, it does not meaningfully participate in the revolution until the synergy phase.

Innovation Premia

With an understanding of Perez’s technological revolutions framework, coupled with the language of network theory, we have identified various mechanisms of mispricing accompanying technological revolutions and are now in a position to more formally clarify what innovation premia is, and is not.

Innovation premia arise not from the mere early adoption of new technologies, but from the misinterpretation of the structural transition they induce. During technological revolutions, the topology of the capital network reorganizes before it is fully perceived. It is within this gap that innovation premia emerge. These premia are not reducible to speculation. While speculative dynamics often coexist, particularly during periods of financial capital expansion, they arise from a distinct mechanism. Innovation premia reflect delayed recognition of structural techno-economic change, whereas boom bust dynamics arise from speculative excess during periods of financial capital expansion. Speculative excess often manifests through financial instrument complexity, at times masking leverage or giving the illusion of diversification and operating in regulatory grey areas, and so on, whereas innovation premia seek to anticipate, and participate in, the new topology within which production capital will be deployed. This underappreciation manifests across multiple dimensions: market, organizational, and behavioural, the last of which applies at the societal, firm, and individual levels.13

This distinction is critical. To view the current environment of AI solely through the lens of a bubble is to completely misinterpret the situation. It’s the wrong frame. We are not merely in a bubble; we are in the midst of a technological revolution. A revolution within which speculative episodes manifest, particularly during the frenzy phase and into the turning point. As such, innovation premia can exist in any space where significant structural reorganization occurs; however, during technological revolutions, the impact is more far-reaching, as all three spheres of change (technological, institutional, and economic) are engaged in radical transformation. While this increases the breadth of opportunities to harvest innovation premia, they are simultaneously occulted from view, as speculative behaviours in the market add noise to the signal.

We are not merely in a bubble; we are in the midst of a technological revolution.

By viewing the current market dynamics in this way, we provide ourselves with a framework in which one can respond proactively, rather than reflexively. Within the bubble frame, the primary focus of investors is on timing an eventual correction, or holding cash in anticipation of future opportunities after the crash. A wait and see posture, while prudent, narrows the field of view. Expanding that frame to encompass the full cycle of technological revolutions does not reject prudence; it broadens the scope for agency. The shift is not away from prudence, but beyond it. Opportunities are not only confined to the aftermath of the correction, but are, in fact, already forming within the ongoing reorganization of the system.14

Harvesting Innovation Premia

Identifying where mispricing is most likely to occur requires us to map and monitor firms tied to emerging hubs associated with the new technology, as well as those likely to lag in adopting it. Detecting and monitoring the diffusion of these structural changes is a first step. As with many insights, early positioning matters, and this is precisely where the multi-depth network technology discussed earlier can provide actionable insight, or at the least, risk assessment.15 Monitoring the form, pace, and nature of customer-supplier relationships at the fringes of the network can provide early reads on the transition to the new technology. Even something as simple as monitoring how distal nodes begin to reclassify themselves, not in GICS, but in their own filings, can be incorporated into the analysis. This is not new. However, the point is not to better categorize a company for neutralization or other such tasks, but rather that the pace of the structural reorganization itself is the signal to monitor. It is the temporal component that contains the relevant information.

Empowered with multi-dimensional network analytics, a wider picture of the emerging techno-economic landscape comes into view. As centrality measures shift across infrastructure providers, complementary industries, financing networks, supply chains, and partnerships, the structure of the new paradigm reveals itself across domains. One approach to monitoring this transition is to dynamically classify nodes based on their degree of adoption or integration into the new technology and distinguish them from those still tied to the legacy system.16 This effectively cleaves the investment universe into emerging and incumbent networks, allowing the former to be monitored as a standalone system while the latter remains in place but gradually reorganizes. For example, the Magnificent 7 and their first-degree relationships can define a proto-network, which can then be expanded in depth and dimensionality. Network analytics then provide a means of quantifying where new centres of gravity begin to coalesce, and where existing ones are in decline. Once in place, we can now monitor how information flows through.

Capital Dynamics

What Perez also highlights is how speculative financial instruments absorb and redirect capital, acting as an additional network layer through which capital flows are mediated. Being able to ingest and interpret capital flows is a common source of alpha for many quants. For example, hedge fund holdings and short interest data have been used to capture sentiment related to individual firms. Once again, we can also employ networks to assess how aggregated flows propagate through the system. What Perez also highlights is how speculative financial instruments absorb and redirect capital. Understanding how these instruments, derivative or otherwise, aggregate can be used to assess risk. As such, another partition becomes possible: productive versus speculative instrument exposure.

One interesting class of financial instruments, not present in any meaningful capacity during the TMT Bubble, is Exchange Traded Products (ETPs). These have the potential to allow a wider array of investors to participate in broader themes associated with the technological revolution, for good or ill. While many ETPs are fixed and tied to legacy paradigm industry compositions, the advent of new, active ETPs allows even retail investors access to dynamic exposure to structural themes. Instead of having to pick a single stock with a high level of risk, the retail investor can purchase exposure to a basket. Active thematic ETPs thus allow investors to be directionally correct, rather than precisely wrong. As daily NAV flow information is readily available, this becomes another avenue through which to assess how flows move between regions, industries, and themes during the technological revolution.

Temporal Compression

As is shown in Figure 1, the diffusion curve of Perez is not a straight line with a constant slope. Rather, the shape is an S-curve, which exhibits a rapid phase of diffusion during the installation period and then flattens out at the onset of, and throughout, the deployment period. It is important to note, however, that a full cycle of a technological revolution takes place over decades. Furthermore, implicit in the overlapping S-curves in Figure 1 (i.e., the grey lines) is that techno-economic paradigms are not smooth transitions from one to the next. As such, we can infer with some confidence that harvesting innovation premia amounts to harvesting long-horizon alpha, yet one with a compressed payoff period relative to the full cycle. Alpha capture compresses in the maturity phase, inasmuch as it relates to the old paradigm. Nonetheless, the unique nature of innovation premia is that it arises from techno-economic structural dislocation, with payoff profiles that can persist for several years. This suggests that opportunities exist for managers with the skill and ability to make longer-horizon investments, yet potentially realize the associated alpha over a shorter period; that is, the liquidity risk often inherent in long-horizon trades may be mitigated in certain corners of the emerging techno-economic paradigm.

Challenges for investors nonetheless arise due to the overlapping nature of the technological diffusion S-curves, especially for those who rely heavily on backtests with deep histories. The techno-economic paradigm in which the backtests are run financial instruments, data availability, prevailing assumptions about the economy, market participants, and so on is inseparable from the analytic framework employed. This creates a trade-off between longer historical backtests with increasingly invalid paradigm assumptions the further back one goes (and thus weaker interpretability), and more consistent assumptions with shorter histories and weaker statistical power. Indeed, alpha models that rely on long histories for training may experience a disconnect as the new paradigm takes hold. The relationships embedded in the data of the old paradigm may weaken as the new paradigm diffuses through the system, including expectations about market participant behaviour and how novel financial instruments may alter sensitivities to shocks. For example, up until roughly 2010 to 2012, ETPs played a relatively minor role in single-stock dynamics. However, as ETP volumes and holdings in underlying assets increased, underlying stock volatility did not simply reflect changes in magnitude, but rather acquired a new structural component.

Many managers already incorporate point-in-time (PIT) data, tools that restrict training to data available at the time, and ensembling methods across multiple horizons and forecasting variables, all of which can help smooth these effects. The point here is not to suggest that all backtests are flawed, but rather to highlight that many foundational assumptions evolve more rapidly during technological revolutions.17 This reinforces the earlier insight that one mechanism of innovation premia arises from a temporal misalignment between the evolving structure of the economy and the assumptions embedded in models derived from the prior paradigm.

Not all systematic analytics are created equal. It will be those managers who recognize the importance of investment in their technology who benefit the most.

Institutional Sphere

Until now, we have kept our discussion predominantly within the economic sphere and now turn to the institutional sphere. Specifically, we focus on the organizational dimension as a legitimate and distinct form of structural mispricing.

As alluded to earlier in the essay, regulatory bodies will, by definition, also lag the pace of diffusion of the new techno-economic paradigm into the economy and society. In Perez’s model, it is usually not until after the crash that regulators are able to effect any meaningful changes. Their role is to stabilize, but they can only do so once they have a clearer picture of the forces that need to be reined in, be they policies tied to speculative financial instruments, labour laws, or otherwise. When it comes to the workforce, much of this is shaped by how organizations themselves adapt to the new technology.

This lag manifests, more specifically, at the organizational level. There exists an organizational dimension to the change that accompanies technological revolutions. Not only are there lags in the adoption of new technologies, but also in how organizations are able to adapt to the realities the new paradigm demands. That is, the more transformative the technology, the more radically the way of doing the job itself changes. Firms that are able to recognize the shift in skill set and mindset required to fully realize the benefits of the new technology will outpace those that fail to do so. Don t believe me? Ask any Blockbuster employee.

Most quants, as a normal course of business, allocate a portion of their risk budget to exploring new and novel techniques to avoid stagnation in model design. So, too, must organizational structures experiment with new technologies to avoid the risk of becoming obsolete. This implies that full participation and enablement will also be subject to a lag, resulting in a form of organizational alpha that can be realized by those most capable of adapting their practices to the new technology, and who may, as in the case of Netflix, become leaders in the next techno-economic paradigm.

Artificial intelligence heralds profound organizational change across multiple dimensions. Consider that a core advantage that has consistently materialized in the information space is the speed with which information travels: it compresses the time to decision-making. From the telegraph to the ticker tape, to the telephone, to the internet, both the speed and volume of information placed into the hands of decision-makers have increased by orders of magnitude. With AI, we now observe a further compression occurring via several channels: the ability of AI to process vast amounts of information into a coherent and consumable format rapidly; the ability to pivot more quickly where software is concerned;18 and, increasingly, AI’s ability to also act on the information directly.

In the final analysis, those individuals able to make the corresponding mental shift in how they operate will find themselves on one side of the divide, whereas those tied to the prior model will see their skill sets rendered increasingly obsolete.

Ultimately, each of the spheres is operated and inhabited by people; it is the human variable where value truly accrues during technological revolutions. Perception of the new paradigm is itself the scarce resource being priced. This operates at all scales: the individual, the firm, and society.

Coda

We could go on, but my purpose here was to be indicative rather than exhaustive; illustrative rather than prescriptive. This started out as a book report after all.

AI, in both its speed of innovation and breadth of application across all spheres of the techno-economic paradigm, presents us with a pivotal moment. Temporal compression of structural change is proceeding at a pace unseen in the past. More importantly, the technological revolution we are witnessing will impact more than just our ability to summarize emails, but will reorganize core structures of the economy and society. Innovation premia is the conceptual lens introduced here to capture the financial expression of this lagging understanding across the economic, institutional, and technological spheres. Those able to see beyond the bubble commentary and glimpse what lies on the other side of the next turning point’s horizon will harvest innovation premia; not by betting on the right firm, but by understanding what the emerging structural paradigm is becoming.19

Moreover, the reader will notice that this essay adopts a more positive interpretation. This is done to add to the conversation about AI, which has hitherto been dominated by discussions of bubble dynamics and crashes. The aim is to provide a contrarian view without being naively contrarian, nor entirely Pollyanna. The risks of a crash are real. The risks associated with decreasing diversification are also real. You can find many of those arguments elsewhere.

It is important to recognize the moment for what it is. While the focus has been on the technology and its large-scale impacts, there is a deeper lesson here. Successfully navigating this particular revolution will not be determined by those firms, or societies, with the best hardware or software, but rather wetware: the collective human capacity to perceive what the new paradigm is becoming. From the analyst recognizing the new classification structure, to the organization that fundamentally changes how it operates within the new paradigm, to the culture that establishes the norms of how the new technology will reshape society, the human advantage is, and will always be, the true fountainhead of innovation premia.

I came across Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages while listening to a podcast with the venture capitalist Bill Gurley. It’s no surprise he was talking about the current technological revolution we are in the midst of and how, in Perez’s model, there is more happening at the moment than simply a bubble : a revolution is upon us. At the same time, I was reading William Zinsser’s Writing to Learn Zinsser (1988), and it seemed only natural to apply his concept of getting into the habit of writing to more fully articulate my own understanding of Perez’s work. What first started out as something of a book review quickly took on a life of its own. I thought about ways for investors to proactively rise to the challenges AI poses, and, for lack of a better term, innovation premia became a lens through which to reframe the moment. This essay is the result of that exercise.

It is often said that a good book leaves the reader with ideas they had not previously considered and, at times, prompts further lines of thought on how those ideas might be applied. Perez’s work did that for me, and I hope that this essay will lead you to her Technological Revolutions as well.

Appendix: Innovation Premia Visually

Acknowledgements

I should note that AI in general is used for the creation of tables, TikZ figures, formatting BibTeX entries, fixing LaTeX class file definitions, a word usage dictionary, to critique, and to double-check grammar. The latter of which, I apparently need more practice with. At no point was AI used to write full sentences, sections, the essay’s core ideas, or any of the conclusions.

References

Cooper, George. 2010. Fixing Economics: The Story of How the Dismal Science Was Broken and How It Could Be Rebuilt. Hampshire, UK: Harriman House.

Goodier, Michael. 2025. Revealed: Thousands of UK university students caught cheating using AI. https://www.theguardian.com.

Kuhn, Thomas S. 1970. The Structure of Scientific Revolutions. Second edition, enlarged. University of Chicago Press.

Menczer, Filippo, Santo Fortunato, and Clayton A. Davis. 2020. A First Course in Network Science. Cambridge: Cambridge University Press.

Newman, Mark. 2018. Networks. 2nd ed. Oxford: Oxford University Press.

Perez, Carlota. 2002. Technological Revolutions and Financial Capital: The Dynamics of Bubbles and Golden Ages. Paperback. Edward Elgar.

Planck, Max K. 1950. Scientific Autobiography and Other Papers. Translated by Frank

Zinsser, William. 1988. Writing to Learn. Hardcover. Harper & Row.

Disclaimer

The views and opinions expressed in this material are those of the author and do not necessarily reflect the views of any firm or organization. This material is provided for informational and educational purposes only, and is intended to support discussion. It does not constitute investment, legal, accounting, tax, or compliance advice. No representation is made that any strategy, tool, technology, or approach discussed herein will be suitable or profitable for any particular individual or organization. Any decisions made, actions taken, or implementations pursued based on this material are the sole responsibility of the reader.

Max Planck is famous for having said: A new scientific truth does not triumph by convincing its opponents and making them see the light, but rather because its opponents eventually die and a new generation grows up that is familiar with it , (Planck 1950).

See, for example, (Goodier 2025). Also note that there exists the case for proper use of AI to enhance the education process, and that it can be used both ethically and to effect. The question for educators is how to remove the temptation of convenience AI brings, versus the work and effort involved in an enhanced experience. This is a different topic, but does highlight the institutional challenges where an old paradigm of regulations and structures are unable to accommodate the new paradigm.

Here I am making the distinction that technological revolutions are the society-wide applied revolution, beyond the theoretical. For example, the steam engine preceding the law of thermodynamics, or quantum theory preceding nuclear energy.

It is worth noting that Perez makes a distinction between financial capital and production capital. In the former, financial capital must be mobile to facilitate the rapid growth in the irruption and frenzy phases, dominating the installation period; production capital is the longer-term stabilizing form that sees new infrastructure developed and dominates the deployment period. More specifically, financial capital is the highly liquid, mobile capital oriented toward short-term returns (e.g., equities, bonds, venture financing), whereas production capital is the long-term, fixed investment embedded in productive systems (e.g., plant, equipment, infrastructure, organizational capabilities). The former serves to allocate and reprice opportunities, while the latter serves to build, operate, and scale the real economy (Perez 2002).

In no way can this section’s brief summary convey the magnitude of Perez’s insights. The purpose of this section is to limit discussion to the core insights of her work to provide the necessary theoretical foundation on which innovation premia resides, and should not be treated as an exegesis of Perez’s Technological Revolutions text.

Tulip Mania, occurring in the Netherlands during the 1630s, is widely recognized as the first recorded economic bubble in history. Albeit, the description of it as a bubble is a post hoc designation following the popularization of the term with the British South Sea Bubble of 1711 1720.

To be clear, this statement of the dominant use case is an observation, not an indictment. Considering the breadth of opportunities to apply that approach to extract alpha, it behooves quants to employ it aggressively. I am simply suggesting more signal remains to be extracted; it’s not this or that, but rather this and that.

To be clear, the point being made is that prudence itself can be applied heterogeneously; some sectors of the economy, having adopted the new technology faster than others, may be ripe for investment despite no crash occurring. Innovation premia reflects the opportunity to capture alpha associated with delayed structural recognition brought on by the new technology, rather than a view on specific companies themselves.

A standard discussion now amongst many quants is how to best employ AI models from third-party providers. The challenge is that the weights on which such models are trained may implicitly contain future information when used in a backtest. How can one be certain, regardless of the prompt, that such information has not influenced the decision-making process, thereby overstating the efficacy of the backtest?

I am reminded of the Type 1 decisions (one-way door decisions) and Type 2 decisions (reversible decisions) of Jeff Bezos here. AI has the potential to transform what was previously considered Type 1 decisions in software design into Type 2 decisions, as the consequence of pivoting is radically shortened with agentic programming. In other words, one-way doors become two-way doors.

While this essay focuses on the opportunities, wise investors also recognize the risks associated with decreasing diversification, as the emerging techno-economic paradigm is broadly exposed to the new technology.